5.2 Future Value of An Ordinary Annuity

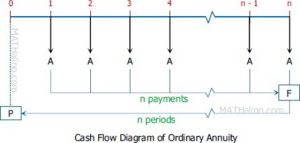

The future value of an ordinary annuity is defined as the amount due at the end of the term that is equivalent to the sum of the future value of all the payments comprising the annuity, with the date of the last payment as the focal date. An ordinary annuity is shown on the time diagram below.

To calculate the future value of this annuity, we need to accumulate each payment at the end of the term. This may be expressed as follows:

= (1 + i)n−1 + (1 + i)n−2 + … + (1 + i)2 + (1 + i)1 + 1

Written this in the other way around, we have:

= 1 + (1 + i)1 + (1 + i)2 + … + (1 + i)n−2 + (1 + i)n−1

This expression is a geometric progression with n terms, where the first term is 1 and with a common factor of (1 + i). Hence, using the formula of the sum of a geometric progression, we can generate the future value as follows:

=

= ![\frac{1[(1+{i})^{n}-1]}{(1+i)-1}](https://umspressbooks.colvee.org/financialmathematicsineconomics/wp-content/ql-cache/quicklatex.com-6b9070bfee0d84879b67476b2e24f3a0_l3.png "Rendered by QuickLaTeX.com")

=

The future value at i of RM1 paid at each period for n periods is often written as:

, read “s angle n at i” where;

, read “s angle n at i” where;

The future value of an ordinary annuity of n payments of RMR each, multiply by R and is written as:

Future value =

A worker is saving RM1000 each year and depositing it into Bank A. How much money will she have at the end of 40 years for her retirement if the interest rate is 9% p.a.?

Find the future value of an annuity of RM1500 payable at the end of each month at i12 = 8% for 10 years.